January 27, 2026

MEMO: States Are Moving Quickly to Disconnect from Trump's Reckless Tax Bill. Will Oregon Join Them?

Dozens of other states are already better insulated from federal tax code volatility or are acting swiftly to disconnect from the most harmful provisions of HR 1. Oregon is, and will continue to be, an outlier if it chooses to take no action and absorb the most damaging provisions of the Republican Budget Bill.

Five Key Takeaways:

1. We’re behind the curve compared to other states in minimizing our exposure to federal tax code volatility.

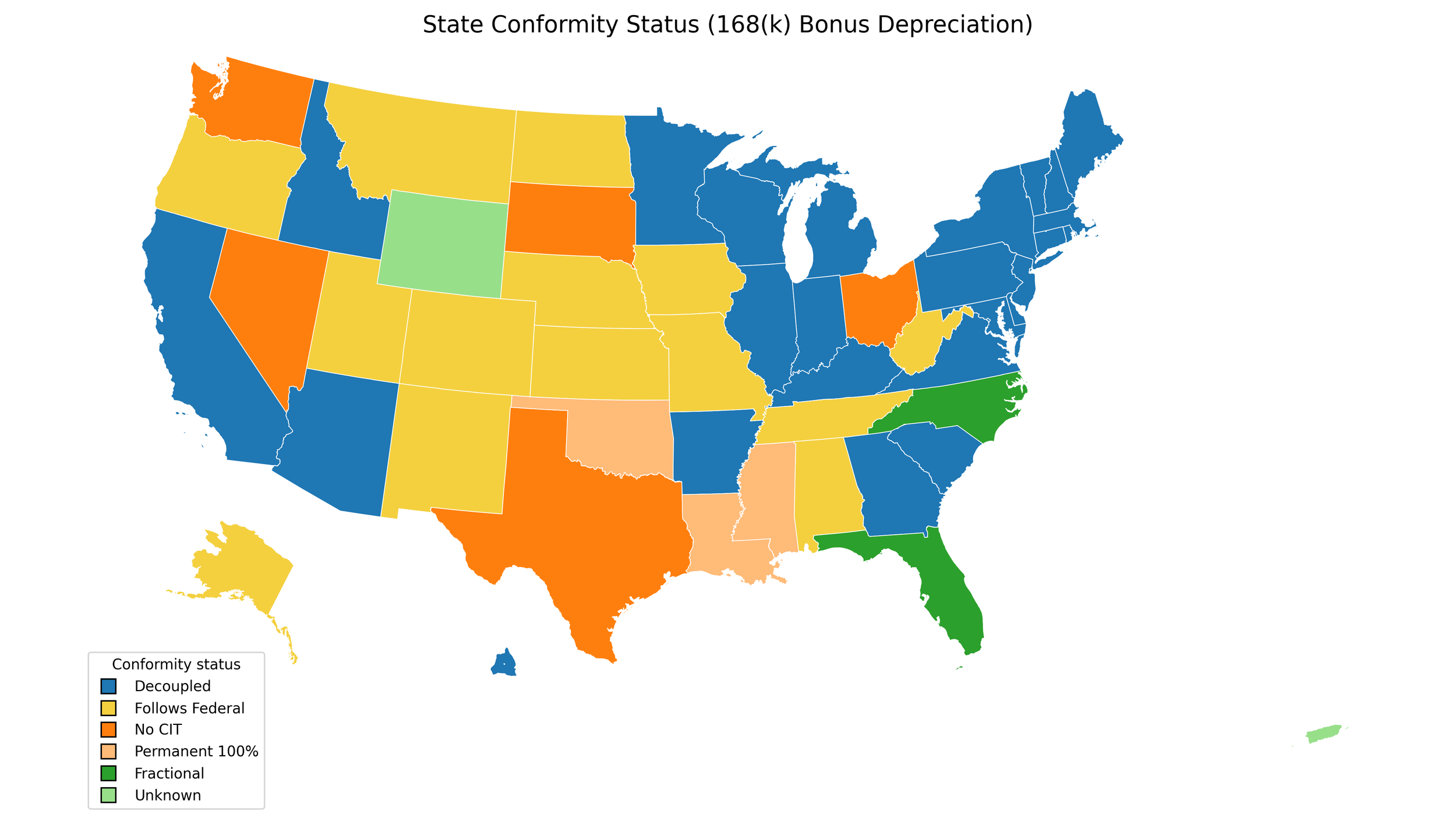

Over two dozen states, including, recently, California, Maine, and Illinois, have selectively disconnected from Business Depreciation provisions.*

More than 20 states have selectively disconnected from tax breaks for global corporations.**

California, Alabama, Mississippi, Pennsylvania, Massachusetts, and North Carolina have disconnected from some tax breaks for wealthy investors.***

More than 20 states with income taxes do not conform to the SALT cap.****

2. For the selective disconnect provisions we are looking at, 39 states, 89% of states (and DC) with income taxes, either never connected or have disconnected from at least one of them

3. Oregon is particularly vulnerable to the negative impacts of the Federal Republicans’ tax code changes. This is because Oregon depends more on income taxes than any other state, and we are one of only three states that both connect automatically and connect to so many provisions within the federal tax law. It’s economic malpractice to maintain full exposure To federal tax code volatility.

4. Oregon has done this before. Oregon’s Legislature selectively disconnected from some of Trump’s 2017 tax code changes in the 2018 session.*****

5. Other states are taking action:

Colorado convened a special session where they made state-specific and federal connection changes, reducing their deficit by around $250-300 million. Notably for Oregon's conversation, this included disconnecting from Foreign-Derived Intangible Income (FDII).

California just passed its newest conformity bill, which aligns to the Internal Revenue Code (IRC) as of 1/1/25, therefore excluding any of the changes in HR1. California has a unique alignment with federal tax law in general, with many individual connections and disconnections. Still, it's worth noting that they remain not connected to FDII, Opportunity Zones, bonus depreciation, Section 179 expensing, Research & Experimental (R&E) expensing, and more.

Maine disconnected from several provisions, retroactive to 2025. Those include not connecting to: R&E expensing (except for certain small businesses), bonus depreciation, tips tax exclusion, overtime tax exclusion, and Section 179 expensing (except for certain small businesses). Lawmakers gave the Governor authority to decouple administratively.

Rhode Island took an administrative path and decoupled from the R&E expensing without needing to pass a law.

Michigan recently passed a bipartisan budget deal that disconnected from depreciation for Qualified Production Property and R&E expensing.

Illinois just disconnected from bonus depreciation for qualified production property and aligned at 50% of NCTI (GILTI).

At the end of 2025, Delaware Gov. Meyer signed into law a bill that will recover more than $300 million for the state by decoupling and modifying the state's connection to key Trump tax provisions — including bonus depreciation.

The D.C. City Council voted to decouple from several OBBBA tax provisions, including the Qualified Small Business Stock exclusion, no tax on car loan interest, full expensing of domestic R&E, and the special treatment for qualified production property.

The Pennsylvania budget's primary tax bill, H.B. 416, decouples the state from three tax provisions in this year's federal budget reconciliation bill: an immediate deduction for R&E expenses, immediate expensing for qualified production property, and a more generous calculation of Internal Revenue Code Section 163(j) 's interest deduction limitation. Shapiro, a Democrat, signed the budget in November 2025 after lawmakers reached a budget agreement months after the state's fiscal year began on July 1. Decoupling from the provisions will prevent Pennsylvania from losing more than $1.1 billion in tax revenue over the next fiscal year.

*Tax Foundation. “Big Beautiful Bill: State Tax Impact.”

**Tax Foundation. “GILTI State Conformity Issues Loom in 2020.”

***Institute on Taxation and Economic Policy (ITEP). “QSBS: Trump Tax Law Threatens State Revenues, Enriches Wealthy.”

****Institute on Taxation and Economic Policy (ITEP). “SALT Cap: Trump Megabill State Revenue.”

*****Oregon Capital Chronicle. “Oregon Democrats Mull Options as Time Runs Out to Divorce State Tax Code From GOP Cuts” (Sept. 11, 2025).